Whole vs. Term Life Insurance in 2026: Differences Explained (+What You Need)

Table of Contents

Table of Contents

Insurance Claims Support & Sr. Adjuster

Kalyn grew up in an insurance family with a grandfather, aunt, and uncle leading successful careers as insurance agents. She soon found she has similar interests and followed in their footsteps. After spending about ten years working in the insurance industry as both an appraiser dispatcher and a senior property claims adjuster, she decided to combine her years of insurance experience with another...

Kalyn Johnson

Sr. Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Brandon Frady

Updated October 2024

Many people come across life insurance when one of their friends or family members becomes an agent and keep pushing a policy product in their face. In most cases, they end up buying some sort of coverage without knowing the details. To avoid getting into this situation, this article will explain to you information of a life coverage, the difference between whole life and term life policies along with many other related topics.

Why Do People Want to Purchase Life Insurance?

Aside from the previous scenario mentioned in the introduction, the Number 1 reason people purchase life insurance is to ensure that in the sudden event of their passing away, their love ones (e.g. parents, spouse, and children) will be left with a solid financial foundation to sustain their lifestyle. At the same time, the life coverage will make sure that the policy reimbursement will be used to pay the estate taxes so that your family will not have owe any money to the government.

For any business owners, your family members are not the only ones to be affected. Your partners, co-workers, and employees all rely on you to various degrees. Should you suddenly pass away, your death can completely ruin the company. It is even more disastrous if you have taken out a loan on your family assets (e.g. your family home and vehicles) to expand the business. Without your company’s income and their inability to pay back the loan, your family will have no choice but to sell the business to recur some money. In most cases, people will take advantage of your family members in this situation and buyout the business at a much lower price than its actual worth. Even if your partners are willing to buy out your share, they may lack the immediate funds to do so. Even if your family decide to get into the business, it will be an extremely stressful time to deal with both losing you and learning everything about the operation within a short time. Knowing firsthand how much dedication and energy is needed to run your company, you definitely do not wish to throw your family into the deep end. Here is the time when a life insurance can protect both your family and your business from financial hardship, pay off any business debt, and allow your partners and family members to decide what is best for everyone.

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

Different Types of Life Policies

Before you jump into shopping for a coverage plan, you should know that there are 2 major categories of life protection plans:

- Term life (sometimes referred to as pure life insurance)

- Whole life (sometimes referred to as permanent life insurance)

What is Term Life Insurance?

Term packages offers a limited time coverage for your dependents should you pass away before the set term terminates. If that occurs, the insurer will honor the agreement to settle your debts and estate taxes, as well as pay your beneficiaries a set amount of money as stated in the contract. These policies can range from 1 year to 30 years.

Common types of level term are:

- Annual renewable

- 5-year renewable

- 10-year

- 15-year

- 20-year

- 25-year

- 30-year

- Term set to an identified age

Types of Term Life Protections

There are 4 types of term coverages:

- Level term: The death benefit of these policies remains the same throughout the whole duration of the coverage.

- Decreasing term: The death benefit decreases by monthly or annual increments over the duration of the coverage.

- Annual renewable term insurance: The death benefit remains the same throughout the whole duration of the coverage. However, for every year, your premium will increase to secure the same amount of death benefit payout.

- Convertible term life: These plans allow the subscriber the flexibility of converting their term life to a whole life policy during an indicated interval of time without needing to provide evidence that they are in good health.

Who Generally Benefits from Buying Term Coverage?

These policies are best for people who do not have a large financial portfolio but wish to secure a form of inheritance for their beneficiaries. This way, your children will have the financial means to provide an even brighter future for the next generation. As home prices escalate in an alarm pace these days, your children and grandchildren can definitely benefit with from the money.

Advantages and Disadvantages of Decreasing Term Policies

Life most people, you may wonder why anyone would choose a decreasing term plan? Here are the advantages why you may want to consider this option:

- It is lower in price than level term plans.

- It usually offers for the biggest amount of immediate death benefit for each premium dollar.

- You wish to have some sort of security to fall back on for your dependents yet you cannot afford a whole life insurance plan.

- You only wish to cover the mortgage of your home and your spouse does not rely on your income. So over the time as you pay off your mortgage balance, you no longer need as much money to pay off that mortgage.

- You are anticipating that you will pay off your debts throughout the years and no longer need this safe net security in the future.

- You are anticipating that your dependents will be graduated from college and find their footing in life that they no longer need this financial security. And as they leave home, your spouse will require less expenditure in daily life since all loans and mortgages will be paid off by that time.

Disadvantages of Decreasing Term Policies:

- Your premium fee throughout the agreed term will generally increase over time. This means that you are paying more for a contract that decreases in value throughout the years.

- This type of plan will not offer any security for your spouse if they solely rely on your income as living expenses and they have no sources of income themselves.

So unless a person has very specific goal they wish to protect (e.g. paying off home mortgage, providing tuition for children’s tuition, paying off the loan taken out to develop business), people usually opt for the level term or convertible term policies.

What Are the Premium Cost for Term Coverage?

Unlike any other packages, the premium is heavily dependent on the subscriber’s age and health at the time of the purchase. In general, the younger you are and the healthier you are, the lower your premium. The next crucial factor is the length of your coverage; shorter the duration will usually be lower priced than longer terms.

However, there are some longer packages that will guarantee you that your monthly payment will not increase during a certain periods of time. For other plans, the company may guarantee you that your rate will only increase to a certain price and plateau afterwards. The last important factor is how much do you want the payout to be? Obviously the higher the death benefit, the more expensive the plan.

People often picture life assurance to be a “luxury” only the rich can afford. It is not the case, a quote example below will allow you to see the approximate cost for a 20-year term coverage plan that is worth $250,000. As you can see, the age discrepancy and whether you are a tobacco user can really change the cost. Surveys done by the industry have found that smokers pay up to 200% more on average for the same protection as subscribers who do not smoke. The example can show you that as you age, the cost discrepancy between smokers and non-smokers can triple or more. One thing for sure, if you want an affordable plan, stop smoking!

| Age | Aerage Annual Term Insurance Premium |

|---|---|

| 25 | $330.33 |

| 30 | $334.54 |

| 35 | $359.78 |

| 40 | $432.36 |

| 45 | $619.42 |

| 50 | $918.91 |

| 55 | $1,455.34 |

| 60 | $2,492.43 |

| 65 | $4,172.01 |

Return of Premium Feature in Term Coverage

Just like any type of coverage, life assurance will only pay out if the subscriber pass away before the package expires. There is no special prize if you outlive your contract. For some customers, they feel that they should be rewarded for living a healthy life and make it pass that expiration date. So compensate for this problem, some insurers have come up with this option called “return of premium” that will allow the subscriber to be refunded their premium after their plan expire. Please note that every company may have a slightly different payback system. For some, they may refund you the whole portfolio cost plus the agreed payout; for others, they will only return the premium cost. If you are considering this option, please ask your agent the details before purchase. One thing we can guarantee you is that adding this feature will drastically increase your premium cost. At the same time, you may lose the flexibility of switching your plan details.

What is Whole Life Coverage?

Whole life policies guarantees to remain effective throughout the subscriber’s entire lifetime or to the maturity date of the plan from the day the plan is activated. There are 3 main categories of permanent life protection:

- Traditional (also referred to as straight life or ordinary life)

- Variable

- Universal

- Variable-universal

- Survivorship (sometimes known as second-to-die coverage)

Within each class, variations is available depending on each provider.

Traditional Whole Life Insurance

Traditional whole life is known as the most basic type of permanent coverage in which you pay a fixed amount of premium per payment period and your beneficiaries will receive the guaranteed death benefit as stated in the contract agreed upon between you and the provider. As long as you keep paying the monthly fee, you do not have to worry that your cost will increase throughout the years or your coverage to change over the years. You may wonder why insurers would agree to not increasing your premium. This is because they charge you a higher rate than the cost of your coverage. This cash difference is then put into a cash reserve (also known as cash value). So by the time you reach to a much older age when your contract becomes more expensive, the insurer will use the accumulated cash value to help cover the cost. Here is an example to illustrate how it works:

You just purchased a $150,000 plan at age 25. Because you have no accumulated any cash value, you will have to pay for the $150,000 coverage cost. Say, when you have reach 30 and you have gathered $15,000 of cash reserve. The company will then use that quantity to cover part of your premium, and you will be paying $135,000 of the coverage. As the reserve continue to accumulate, the price of the insurance will continue to fall.

Variable Life Insurance

In essence, it is very similar to the traditional permanent policies. The difference is that holders can decide the utilization of the cash value. Instead of putting it back to cover the cost, customers can choose to put the money into an investment portfolio account managed by the provider. The earnings can then be used to either lower your monthly cost or added to the death benefit payout. However, please note that investments do not always do well. If the portfolio end up losing all the money, your reserve will be gone. So there is always an element of “what-if” in this type of plan.

Universal Life Insurance

This category of protection coverage provides policyholders with the most flexibility than any other type of permanent policies. You are allowed to increase your payout amount as long as you pass a medical examination to proof your health has not changed since the initial agreement. Like the traditional coverage plans, you get to open a cash value account and accumulate the reserve and earn the market interest rates. After accumulated to a certain level, you will have the option to keep putting money away, pay less premium, or even skip some payment as long as you maintain the minimum annual payment over the year. So in cases where your financial status changes and you are tight on your budget, you can still keep your portfolio effective when you need to skip a few payments.

Variable-Universal Life Insurance

These plans have combined the features of both universal and variable coverages to give you maximum flexibility in plan changes as well as cash value utilization. You will be allowed to make changes in death benefits, and use the savings for investment, lowering your cost, skip payments, and even put towards a higher payout for your beneficiaries.

Survivorship Life Insurance

This type of plan is used to cover 2 lives within 1 policy. It is best for spousal situation where if one person passes away, the other person will receive the death benefits. It is an alternative affordable way to insure 2 people at the same time than purchasing 2 separate policies.

Who Generally Benefits from Buying Whole Life Insurance?

Because permanent life coverages are more expensive than term assurance packages, they tend to be most beneficial for people who are not tight on budget and have maximized their annual purchase of 401(k) plans, Roth IRA, IRA options, and 529 plans. Although you cannot deduct the premium since it is a personal expense, your earnings from the cash value investment will not be taxed as long as you do not take out more than what you paid as your annual fee. On the other hand, the earned interest from the deposit is still regarded as taxable interest income. To avoid being penalized, it is best to consult your portfolio agent, your accountant, or your tax prepare for more information.

Average Premium Cost of Whole Life Policies

As stated before, permanent protection packages tend to be more expensive. To give you an estimate of the average cost, here is a chart of how much it will cost if you purchase a package at different age bracket:

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

Pros and Cons of Term and Whole Life Plans

Although on the surface whole life coverages seem like an investment for the top earning crowd in society, you may want to take deeper look at both term and whole packages before making your decision.

Pros of Term Packages

- Most affordable types of protection you can purchase.

- The rules are easy to understand – you pay your fee and your provider promises to compensate your beneficiary the agreed amount of money if you pass away while the coverage is active.

- The payout is predictable. There is no hidden cost to worry about.

- You can cancel the agreement at any time even before it expires. You will either need to re-negotiate the deal, shop around for a new plan, or convert the existing plan into a permanent package.

Cons of Term Packages

- Once the term expires, your monthly fee significantly increases.

- If you stop paying your dues and the policy lapse, the agreement between you and the insurer is no longer effective.

- Once the agreement terminates and you are still alive, you get nothing back unless you have purchased the return of premium feature.

Pros of Whole Life Packages

- Once the plan becomes effective, it never expires as long as you keep paying the minimum amount of due as stated by your company.

- Your rate will never increase. And if you choose to use your cash value towards covering your premium, your rate can even decrease in the future.

- Part of the due you give to the insurer can be put away as an investment or put towards your cost.

- Can be used as a relatively safe way to invest for yourself and for your beneficiary.

- You are allowed to take cash out without paying tax penalty for the action like IRA and 401(k) accounts.

- The cash reserve works as a safety net that allows the plan to be effective even if your premium lapse.

- The beneficiaries will always receive the death benefit no matter when the policyholder keeps paying for the premium until the person passes away.

- If you do terminate the contract, your cash value will be refunded back to you.

- Even if you choose to invest your cash value, it is highly unlikely to suffer market loss as your portfolio includes low risk investments such as mutual funds and other similar programs.

- Your money will grow every year. With the tax-free, economy-driven growth in your investment along with yearly interest in your cash value, your portfolio will continue to increase in value throughout the years.

- The dividends you earn from the investment are not taxable. Although the amount depends on your portfolio and the amount you invested, it is always nice to have extra non-taxable money coming back to you.

- You can gain access to the money reserve whenever you want without penalty as long as you do not take out an amount that is more than your annual contribution.

- Accelerated death benefit can be a life-saver when you are diagnosed with a terminal illness and you require quick cash for your medical expenses to stay alive. You will have the option to take out a percentage of the death benefits to pay for these bills without worrying about your financial difficulties during this already stressful situation (More on accelerated death benefits later in this article in the section “What is Accelerated Death Benefits?”).

- You can use the package to borrow money to develop your business or other investments to accelerate the accumulation of your wealth.

- Unlike cash, properties, jewelry, and other items that are taxable by the government, the death benefit is left to your heirs without any taxation. So if you have a large accumulation of wealth and you wish your beneficiaries to avoid being taxed in the transferal of your inheritance, life protection portfolio is a good option to evade the problem.

Cons of Whole Life Packages

- Generally expensive.

- Policyholders tend to buy less coverage than they truly need.

- Much more complicated to purchase as there are many options to customize your plan to suit your goals and needs.

- Require some knowledge on finance and investment.

- There can be an element of seeing your payout shrink due to investment loss from your portfolio.

- The cash value gain and loss, and your interest growth from the reserve accumulation can make your tax preparation much more confusing.

- How much growth in your package will depend on how well you set up your foundation during the early years of the plan.

Summary of Strengths and Weaknesses of Both Type of Policies

| TYPE OF POLICY | PREMIUM | FACE AMOUNT | CASH VALUE |

|---|---|---|---|

| TERM | Low; Increases with Age | Renewable into old age | None |

| WHOLE | Same throughout Policy | Level (Can’t be changed) | Yes; No Investment Option |

| UNIVERAL | Flexible | Level; (Can be changed) | Yes; No Investment Option |

| VARIABLE | Same throughout Policy | Level; (Can’t be changed) | Yes; Investment Option |

| VARIABLE UNIVERSAL | Flexible | Level; (Can be changed) | Yes; Investment Option |

What is Group Insurance?

Certain companies may offer their employees a chance to purchase life assurance under a group plan for a discounted rate or the companies are willing to chip in as part of the worker benefits. For these plans, physical examination is usually not needed. For many states’ regulation on group plan, employees must have the right to convert their proposal into a permanent life policies once the existing group policy reaches the termination date.

What is Accelerated Death Benefits (ADB)?

This optional add-on feature allows the policyholder to take out a cash advance against the payout when they are strap for cash for treating a terminal illness. As medical treatments and hospital stays can be extremely expensive even with health insurance benefits, some individuals have the option to use part of the death benefits to pay for the expenses needed to keep them alive. If you are interested in this feature, have a talk with your agent before the purchase. Depending on the company and on the packages, some plans already come with this benefit whereas others require a small add-on fee.

When Can I Request This Payment?

In order to qualify for ADB, you must first meet the requirement that you are suffering from an illness that is included in the acute, terminal, and catastrophic illnesses list in the contract guidelines.

- Acute Illnesses – e.g. severe heart diseases, HIV, hepatitis B/C

- Terminal Illnesses – Any illnesses with a life expectancy of less than 24 months.

- Catastrophic Illnesses – Any illnesses that require extreme treatments e.g. organ transplant, amputation, leukemia, heart attack, stroke

Can my Beneficiaries Still Collect Any Money if I Took Out an ADB?

This question hinges on how much you took out as your payment because this sum of money is deducted from your death benefits to your beneficiaries. So the more money you took out, the less will be paid out to them. And in extreme cases where you took out the whole amount, your beneficiaries will have nothing.

What Plans Offer Accelerated Benefits?

These days, many plans do have this option. A $25K permanent life package should already include this benefit. Please note that not all term plans will offer this option. If you are interested in this emergency cash payment, ask your agent during the counselling session to make sure your selection includes this advantage.

Can My Insurer Cancel My Plan If They Know I Developed an Illness?

Never. The company is legally bind to keep your protection active as long as you keep up with your bills and the term has not terminated. If any company attempts to deny you coverage in this circumstances, contact your state’s agency and report of such activity.

How Much Money Can I Take Out for My Coverage?

The general ADB advance cash withdraw ranges between 25 to 95% of the death benefit. The actual sum can range depending on your assurance’s value, your residing state regulation, and the contract terms. For certain companies, they will go as far as allowing a 100% withdrawal in extreme circumstances. Please note that depending on your provider’s guidelines, there may be a service charge applied on top of the withdrawal. The good news is federal income tax regulation states that accelerated death benefits are not taxable. However, in order to qualify for the exemption, you must be certified for the health status to justify the omission. Also note that the withdrawal method can also differ based on the company’s regulations. For some, they may pay out as monthly stipends, others will pay in a lump sum, and there will also be ones who will allow you to choose.

Are There Better Options Than ADB?

This option is regarded as the last option. Before considering this drastic measure, please consult with your health agent to see if you qualify for Medicaid. Under the United States Department of Health and Human Services regulations, you should not be penalized for having a life plan and your eligibility for Medicaid should not be affected by the plan ownership, your decision to without ADB, or your withdrawn ADB funds. ADB is not considered as income.

What If I Do Not Die After Taking Out an ADB?

Once the provider issues your funds, you are not obligated to return the money. However, filing a false claim to retrieve the funds can land you into deep trouble. The company will have the right to sue you for fraud in criminal court, demand the money back, drop your coverage, and sue you in civil court for the expenses they have incurred in handling your portfolio and emergency claim.

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

Which Type of Coverage Should I Purchase?

Many people often recommend that term policies is the better choice of the two because it is much more affordable. However, what can save you some money now, can cause you to receive nothing in the future. In order to answer this question, you must first examine 2 questions:

- What is your current financial situation?

- What exactly are you trying to protect (e.g. your home mortgage, your spouse, children’s tuition situation, your company’s future, your accumulated wealth)?

Your Financial Situation:

If you are currently struggling financially, but you are married and have children, obviously the best choice will be to purchase a term policy. Having said that, will you be satisfied when you outlive your coverage and receive nothing in return? If not, you probably may want to consider a more flexible plan that will allow you to convert your existing package into a permanent plan when your income and financial status become more stable in the future.

Your Purpose:

If the goal is ultimately to ensure your spouse and your children will have a safety net of money to fall back on before they can finish paying off the home mortgage, complete their college studies and become independent, and there is no other purpose for the coverage, then term life will be your choice. However, if you already have a firm financial foundation that will secure your love ones’ futures, and you are thinking of ways to grow your wealth and leave behind some money for your children and even grandchildren, then permanent life policies will be your optimum choice.

Understanding the Cost Of Life Protection

You may wonder how exactly a quote is calculated, how much do companies actually make off from the package, and how much can you talk down from the initial quote price. Here is a breakdown of the breakdown of how the cost is tabulated for a portfolio. The rate is based on 3 main factors:

- Mortality

- Interest

- Expense

Mortality is the estimation of how long a policyholder will live depending on their individual risk factors combined. Each company has their own charts to assess how likely they will need to payout for a certain group of individuals who share a specific risk factor (e.g. tobacco usage, age, family history of certain diseases, gender…etc.).

Interest is the amount of interest earnings the company can earn from investing your premiums in various investment platforms such as stocks, bonds, real estate purchases, mortgages, and precious metal purchase.

Expense is the cost of running the company. This includes salaries of all the employees, company rent, postage fees, legal fees, and advertisements. This is why larger size companies tend to charge you a more expensive premium; it is not just because they are more reputable, they require more money to keep the company operation going smoothly.

Mortality Factors that Reflects on Your Premium

Just like any other type of protection, the cost of the coverage is a straight reflection of the your risk as a policyholder. When compared to a series of standardize charts of the average customers and their chances of making a claim, you will need to pay more if you appear to be in the high-risk group of subscriber. But on the other hand, if you appear to be in the low-risk end of the spectrum, you will be rewarded with a lower premium than the average rate. According to a survey on the 5 most important factors being examined in the application, these 5 things immediately take priority:

- Age

- Gender

- Value of the policy

- Policy type

- Use of tobacco

Amongst these 5 main deciding issues, age and gender take the upmost priority. You may wonder why does gender have to do with premium cost? According to medical research studies and surveys, the average life expectancy for females is 81.2 years and males is 76.4 years. Based on the statistics, men are much more likely to file a claim than women. Second, men tend to be in higher-risk occupations such as firefighters, construction workers, miners, logging, roofing, fishing, machinery maintenance. Third, men tend to be less careful with their diet and more likely to develop heart diseases. Also, men have the reputation to live a more adventurous lifestyle (e.g. skydiving, drive luxury speedy race cars, rock climbing, deep sea diving, competitive sports, hand gliding) and testosterone-driven risky behavior. Although women are becoming just as adventurous as men these days, the industry still maintain a somewhat stereotype of the gender bias in risk assessment. Consequently, males have to pay more. To illustrate the rate difference, here is a table of the average premium cost of males versus females.

AVERAGE MONTHLY PREMIUM COST OF DIFFERENT PLAN DIFFERENCES BETWEEN MALE VS. FEMALE

| AGE | MALE | FEMALE | ||||

|---|---|---|---|---|---|---|

| $10k | $25k | $50k | $10k | $25k | $50k | |

| 10-YR TERM | ||||||

| 20 | $76 | $106 | $168 | $70 | $97 | $143 |

| 30 | $83 | $115 | $170 | $80 | $105 | $150 |

| 40 | $98 | $140 | $220 | $93 | $130 | $200 |

| 50 | $166 | $280 | $500 | $149 | $245 | $430 |

| 60 | $329 | $702 | $1345 | $275 | $492 | $920 |

| 20-YR TERM | ||||||

| 20 | $91 | $141 | $203 | $83 | $129 | $193 |

| 30 | $109 | $155 | $245 | $100 | $140 | $214 |

| 40 | $132 | $208 | $355 | $124 | $182 | $305 |

| 50 | $269 | $504 | $930 | $223 | $372 | $685 |

| 60 | $638 | $1308 | $2555 | $465 | $900 | $1735 |

| 30-YR TERM | ||||||

| 20 | $126 | $201 | $369 | $102 | $178 | $289 |

| 30 | $147 | $225 | $385 | $125 | $190 | $315 |

| 40 | $204 | $342 | $620 | $167 | $278 | $495 |

| 50 | $403 | $798 | $1535 | $316 | $588 | $1115 |

| PERMANENT | ||||||

| 20 | $417 | $840 | $1505 | $370 | $727 | $1315 |

| 30 | $518 | $1126 | $2063 | $439 | $982 | $1743 |

| 40 | $733 | $1592 | $3015 | $623 | $1332 | $2545 |

| 50 | $1105 | $2425 | $4570 | $941 | $2050 | $3950 |

| 60 | $1709 | $3905 | $7645 | $1499 | $3402 | $6610 |

As you can see in the sample premium chart, the age makes a huge difference in the rate. For the same amount of payout benefits, you would be paying much less if you make the purchase in your early years when you are more likely to be healthier than later years when you are more prone to various health issues. How much you want as your death benefit obviously dictates how much you will have to pay as the subscription fee. Obviously a lower payout will correlate with a more affordable payment versus a large payout will correlate with a high rate. And believe it or not, whether you smoke or not can drastically change your premium rate. As medical studies have shown tobacco usage as the main leading cause to various illnesses, companies view smoking as a sign of early death. The chart below can demonstrate how much of a difference the rate is between smokers versus non-smokers. By being a non-smoker, you are more likely to enjoy a rate that is lower than the average premium cost. On the other hand, smokers will be expected to pay a much steeper price hike due to their habit.

| AGE | MONTHLY TERM PREMIUM (NON-SMOKER) | ANNUAL TERM PREMIUM (NON-SMOKER) | MONTHLY TERM PREMIUM (SMOKER) | ANNUAL TERM PREMIUM (SMOKER) |

|---|---|---|---|---|

| 25 | $27.53 | $330.33 | $55.71 | $668.54 |

| 30 | $27.88 | $334.54 | $60.17 | $721.99 |

| 35 | $29.98 | $359.78 | $67.42 | $809.02 |

| 40 | $36.03 | $432.36 | $97.95 | $1,175.35 |

| 45 | $51.62 | $619.42 | $156.80 | $1,881.55 |

| 50 | $76.58 | $918.91 | $233.21 | $2,798.50 |

| 55 | $121.28 | $1,455.34 | $372.47 | $4,469.64 |

| 60 | $207.70 | $2,492.43 | $555.73 | $6,668.71 |

| 65 | $347.67 | $4,172.01 | $988.32 | $11,859.78 |

More Factors to Consider

After you go through the 5 factors with an agent, you will receive a preliminary quote on your premium cost. However, this is not the end of the deciding factors. Next, you will be asked a series of questions for the company to better assess whether you are a low-risk or high-risk customer. In general, the inquiry will consists of topics such as:

- Your health history – Having previous health history may actually make insurers deny your applications or charge you an extremely high premium plan with the clause that if your death is related to such illnesses, the company will not need to honor the agreement and pay the death benefits.

- Your family health history – If your immediate family members have a history of certain illnesses such as cancer, cardiovascular-related diseases, or diabetes, your rate may become higher due to your higher probability of developing such health issues.

- Driving habits and records — Have you receive any traffic violation tickets recently or any incidents of DUI? Did you ever have your license revoked? Do you own high-end luxury race cars? Occasional traffic tickets may not affect the quote. But serious offenses such as DUI will make you a higher-risk customer.

- Your criminal record – Companies may overlook misdemeanors charges. But if you have any felony charges against you, companies may decline your coverage.

- Your occupation and possible hazards involved – If you work in construction, commercial fishing, logging, mining, or other high-risk occupations, your quote will become higher.

- Your lifestyle and hobbies – Dangerous hobbies such as scuba diving, sky diving, and rock climbing can make your rate go up.

Even More Health-Related Questions and Medical Exams

In order for providers to ensure they are not being manipulated in any way, they carry out a vigorous questionnaire concerning your physical health issues and may request for a medical examination depending on the application guidelines. Here are the most common topics asked in the application process:

- Your weight and your body mass index (also may known as height-to-weight ratio). This question may work in your favor or work against you depending on whether you are physically fit or not. In extreme cases where an individual is classified as severe obese, the insurer may decide to deny coverage.

- Medication check will be on the list of inquiry. In order for your application to be considered, you will be required to agree on their investigation of your prescription record. This is to prove that you do not have any hidden illnesses you decided to omit from the application process.

- A checklist of all physical and mental illnesses you are certainly being treated or have a history of being treated. Anxiety disorder, eating disorders, sleep apnea, elevated cholesterol level, hypertension, diabetes, elevated liver function, HIV/AIDS, hepatitis B/C – these are just some of the listed illnesses on the application.

- You have a history of alcoholism. Depending on your rehab history, the provider may even decide to drop your application in extreme cases.

- You have a history of substance abuse. Marijuana usage is still considered a “drug” by federal laws. So do not be surprise if your rate suffer a hike from your medical or recreational usage of cannabis. Depending on the company guidelines, they can even reject your coverage based on this reason.

- Physical examination is not a must for certain companies. But if your company do require a medical exam, you can expect to perform these tests:

- – Measuring your blood pressure

- – Verifying your height and weight

- – Blood test to test for blood glucose level, liver functioning, cholesterol level, hepatitis B/C, HIV/AIDS

- – Lung functioning examination

- – Heart functioning test

Rate Differences in Different States?

Yes, rates differ depending on where you live. By checking their mortality tables and comparing your region and state with other states’ payout statistics, a company may increase or decrease the average premium rate based on how much premium they take in versus how much claims they have to pay out. Here are some causes that may affect your region’s rate difference:

- Whether the area is known to have a higher rate of obesity

- Whether the area has a higher frequency of serious natural disasters such as flood, tornado, and earthquakes

- Whether the area is prone to deadly illnesses or diseases (e.g. cancer near nuclear power plants, black lung diseases in coal mining regions)

- Whether the area is known for high crime rate

- The amount of policies that have been purchased in the region

Consumer Protection Regulations

What you should know is that each state differs in the regulations for life insurance industry. Because the sales is not regulated by federal agency but state agencies, there can be different laws to mandate specific minimal coverages, how much companies can charge for a package, the customer satisfaction free-to-look time frame, grace periods, underwriting process, customer privacy rights, medical examination requirement, risk factor fairness, and payout of death benefits. Having said that, each state does have a full set of laws to uphold the standards of providers and their agents and to protect customers’ privacy. So before you shop around for a plan, it is always a great idea to visit your state’s life regulation agency for information. They will have a series of guides to help you understand what is acceptable and unacceptable in the application process. To make this process easier, here is the contact list of all the state insurance departments:

| STATE | WEBSITE | TELEPHONE # |

|---|---|---|

| Alabama | https://www.aldoi.gov/ | 334-269-3550 |

| Alaska | www.dced.state.ak.us/ins/ | 800-467-8725 |

| Arizona | www.id.state.az.us | 800-325-2548 |

| Arkansas | 501-375-9151 | |

| California | https://www.califega.org/ | 323-782-0182 |

| Colorado | www.colorado.lhiga.com | 303-292-5022 |

| Connecticut | www.ct.gov/cid/ | 800-203-3447 |

| Delaware | https://insurance.delaware.gov/ | 302-674-7300 |

| Florida | www.floir.com | 850-413-3140 |

| Georgia | https://www.gaiga.org/ | 770-621-9835 |

| Hawaii | https://cca.hawaii.gov/ins/ | 808-586-2790 |

| Idaho | www.doi.idaho.gov | 800-721-3272 |

| Illinois | www.insurance.illinois.gov | 217-782-4515 |

| Indiana | www.inlifega.org | 317-636-8204 |

| Iowa | www.iid.state.ia.us | 877-955-1212 |

| Kansas | www.ksinsurance.org | 800-432-2484 |

| Kentucky | www.klhiga.org | 502-895-5915 |

| Louisiana | www.ldi.la.gov | 800-259-5300 |

| Maine | www.maine.gov/pfr/insurance/ | 380-300-5000 |

| Maryland | www.mdinsurance.state.md.us | 800-492-6116 |

| Massachusetts | www.mass.gov | 800-272-4232 |

| Michigan | www.milifega.org | 517-339-1755 |

| Minnesota | www.mn.gov/commerce/insurance/ | 651-296-4026 |

| Mississippi | www.mid.ms.gov | 800-562-2957 |

| Missouri | www.insurance.mo.gov | 800-726-7390 |

| Montana | www.mtlifega.org | 262-965-5761 |

| Nebraska | www.doi.nebraska.gov | 877-564-7323 |

| Nevada | https://www.doi.nv.gov/ | 888-872-3234 |

| New Hampshire | www.nh.gov/insurance/ | 800-852-3416 |

| New Jersey | www.state.nj.us/dobi/ | 800-446-7467 |

| New Mexico | www.nmlifega.org | 505-820-7355 |

| New York | www.dfs.ny.gov/ | 800-342-3736 |

| North Carolina | www.nd.gov/ndins | 800-247-0560 |

| North Dakota | www.nclifega.org | 919-833-6838 |

| Ohio | www.insurance.ohio.gov | 800-686-1526 |

| Oklahoma | www.oklifega.org | 405-272-9221 |

| Oregon | www.cbs.state.or.us/ins/ | 888-877-4894 |

| Pennsylvania | www.palifega.org | 610-975-0572 |

| Rhode Island | www.dbr.state.ri.us/divisions/insurance/ | 401-462-9520 |

| South Carolina | www.sclifega.org | 803-276-0271 |

| South Dakota | www.dlr.sd.gov/insurance | 605-773-3563 |

| Tennessee | www.tnlifega.org | 615-242-8758 |

| Texas | www.txlifega.org | 512-476-2101 |

| Utah | www.insurance.utah.gov | 801-538-3077 |

| Vermont | www.vtlifega.org | 802-249-0284 |

| Virginia | www.scc.virginia.gov/boi/ | 877-310-6560 |

| Washington | www.insurance.wa.gov/ | 800-562-6900 |

| West Virginia | www.wvlifega.org | 304-733-6904 |

| Wisconsin | https://oci.wi.gov/Pages/Homepage.aspx | 800-236-8517 |

| Wyoming | wyoming.lhiga.com | 303-292-5022 |

| Washington D.C. | www.dclifega.org | 202-434-8771 |

Take Advantage of Free-Look Periods

Just like any type of insurance, there is a free-look period that allows new subscribers the right to reassess and refund their purchases. This period differs from state to state (usually 10 to 15 days). If you do decide to cancel the plan within this time limit, your insurer must refund you the whole purchase without keeping any amount.

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

6 Most Common Reasons Your Application Gets Rejected

Having money does not necessarily mean you can buy protection. As long as you are labeled as a high-risk potential customer, an insurer may choose to turn down your application just to be safe. Here are the 10 most common reasons for a rejection:

-

- Elevated cholesterol and obesity combo. This combination points towards early onset of cardiovascular diseases, stroke, and death.

- Income restriction. This is a hidden sad fact that companies may turn down your application if your income falls below a certain amount. The reason behind this guideline is that insurers do not want to issue many small policies that end up cashing out and clogging up their company running expenses. Another reason is that they assume if you make less than a certain amount of money per year, you are very unlikely to be able to afford a $50K bundle.

- Risky occupation. Some providers like to play it safe and deny coverage for people with certain high-risk jobs. These are the top 10 jobs most likely to be reject by insurers:

- Workers in logging industry

- Fishermen and workers in commercial fishing industry

- Pilots

- Roofers

- Steel and iron workers

- Recyclable material collectors

- Installers and repairers for electrical power lines

- Commercial truck drivers

- Ranchers, farmers, and workers in related agricultural industry

- Construction workers

- Cancer history. Although you have been successfully cured of cancer, providers see you as a high-risk individual who is much more susceptible of going into remission. Depending what type of cancer you had, they may decide to turn your application down. In most cases, if you suffered from minor forms of cancer such as skin cancer, your insurer will still agree to cover you. However, for serious types such as liver cancer or breast cancer, the chances of being accepted is very unlikely.

- History of being declined by other life companies. Just like other types of assurance packages, once you get rejected, your portfolio will be “blacklisted”. Although it does not mean you can never get a life protection plan ever again, it means that the process may become harder.

- Abnormal liver function. This is one thing that many people do not notice unless they have annual medical examination. In most cases, applicants find out when they get turned down in the process. Having elevated liver function does not even necessary mean you have serious liver problems. The condition can be as little as having alcohol or various medication that temporary induces this situation. On the other hand, because liver diseases are often deadly, companies will assume the worst and reject your application.

What Happens If You Get Denied Coverage?

If you receive this news, find out the exact reasons for the application rejection. Under the state regulations, you have the right to know this information in specific written form. You also have the rights to get a copy of the physical exam records used by the provider to access your eligibility. Go through all these information and even consult second opinion on the data (results can be wrong). If you believe that they may have made a mistake on the information or you wish to clarify of the circumstances, call your agent and ask if you can ask for reconsideration by providing additional information or further physical exams. Even if they do not allow reconsideration, you should contact them that the results in the database are incorrect so that other companies will not receive the same information and turn you down as well. If you do decide to apply with another company, let them know of the error from the previous application.

Things to Know Before Purchasing a Life Coverage

-

-

- Know your physical health. Instead of going through the whole process then to be rejected based on a curable physical problem, get a medical routine checkup and find out ahead of time. This will not only make your application more straightforward but also even lower your rate.

- Consider your needs and purposes. It never hurt to consult an agent. They are here to provide information about their available plans and help you find out what type of plan and how much coverage you will need.

- Calculate the Amount of Benefit Needed and How Much You Can Afford. This question hinges on whether you are the sole breadwinner in the household. Typically a plan should cover your final expenses, debts, and other things such as your home mortgage, your spouse’s living expenses, and your children’s tuition fees. In general, experts recommend that the plan should be between 10 to 20 or even 30 times of your annual salary. But the reality is how much can you pay as your monthly or annual premium? Instead of finding out later that you cannot afford the payment, find a medium point where the plan will satisfy both requirements.

- Do not forget to calculate the expenses in handling your death. You may leave behind medical expenses, debts, and annual tax that can amount to quite a number. On top of that, there is the burial and funeral costs, estate taxes, and lawyer fees to consider. Remember to add these items into your coverage costs.

- Learn about your rights as a policyholder. Not all companies and plans are created equal. It is better to find out your rights than to know that you have been taken advantage throughout the years and not receiving the benefits at the end.

- Your beneficiaries do not have to be your dependent or financially dependent. You can name anyone you wish. Some people even have named a certain non-profit foundation, a hospital, or even a college as the beneficiary.

- Consult with an accountant, financial advisor, and investment advisor. If you are purchasing a permanent life assurance, unless you are knowledgeable in financial growth and venture, you definitely should consult with an expert about how to set up your cash value and investment portfolio in the early years to maximize financial growth and benefits.

- You cannot purchase a policy for someone else without proof. If you want to buy a plan in another person’s name, you will need to prove that you are related to this person, you rely this person’s income as your only source of life expenses, and you will not be able to support yourself financially when this person passes away. Beside these basic requirements, you will also need to receive this person’s permission, the person’s background back and medical history (they have to sign a consent form to allow the release of their private information).

- Always window shop and compare quotes.

Each company has its own strength and weaknesses. And some providers are known to be more lenient with certain risk factors than others. Shop around to see which company will give you the best deal and most benefits in return. - Purchase from an independent broker. Although you may need to pay a little for the service, it can save you a lot of time in comparing policies and companies. These brokers also know all hidden advantages and disadvantages as well. For example, if you are a smoker, they may suggest to you certain companies that have a more friendly view towards tobacco users. And if you are a high-risk customer, they will know which companies will accept your application.

- Have a lawyer read through your contract.

If you have any trouble understand the terms in the contract, do not hesitate to have a lawyer read over the details. Make sure that you are okay with all the things said in the underwriting. - Understand the renewal or conversion process. Know everything you can about the process, what will happen to the benefits, and how will that affect your premium. You should also ask what will happen if your health has deteriorated during the process; will they still accept your coverage?

- Always write down the license number and number of the agent you are doing business with. These days, leave nothing to chances. Often if there is a problem in the underwriting and you need to contact the company, they will immediately ask who is your agent and their information. Although unlikely, some sketchy companies may shy away from the problem if you cannot provide these information.

- If you do not like the agent, switch. If an agent intimidates and pressures you from the beginning, you are probably not going to have a great relationship with them down the line. Find an agent that will work with you based on your needs and not on upsell you to get a greater commission.

- Never lie on the application. You may think that you can get away from omitting certain health issues and background information on the application. For health condition, a physical exam can pretty much tell right away if you are withholding certain information. For example, if you are a smoker, had a history of drug use, or had a history of heavy alcohol consumption, the condition of your lungs, liver, and heart can easily let the insurer know if you are telling the truth. As for your background information, even if you can get away in the application process, if later they find out the truth, the company will have the right to terminate the contract without refunding your premium or pay the death benefits to your family.

- Do not sign on a blank or incomplete form and check. This actually is a sign where the agent or the company is pulling a certain trick up their sleeves. Leave immediately if this situation arises and contact your state’s Department of Insurance of the incidence.

- Always keep your contract and other paperwork in a safe place. If your beneficiaries cannot find your policy and contract, it will make the claiming process much harder. And if you do decide to keep the plan a secret, your heirs will never know until they come across the paperwork. Under the state law, the company is legally bind to find your beneficiaries after your death and proceed with the payout. However, companies tend not to search never hard (or never at all) and usually leave the heirs to surface themselves.

- Keep all your receipts and letters from the provider. As a proof that you are always on time with your payments, always keep all your receipts. There is always errors and mishandling situations that can create a lapse in the premium payment. For term plans, that can become a problem and a way for companies to drop your coverage.

- Review your terms every year. A lot can happen every year. Your income can double, your family can grow, and your family expenses can change. Review your financial needs and rethink whether the policy still covers your needs and purposes.

- You can have more than 1 life coverage. As a matter of fact, business owners and people with a substantial amount of accumulated wealth often have several policies for different needs and purposes. Business owners often will have plans that will protect their companies and their partners and separate plans for their personal family needs. Individuals can have separate coverage devoted to specific beneficiaries to avoid family disputes.

-

How Can You Trust a Company?

There is always a question of doubt when it comes to sinking monthly payments into a product that you will never see yourself. Will your beneficiaries actually get to receive the benefits? To lessen the risk and quiet the qualms, here are some helpful tips:

Research the Company’s Financial Strength Ratings

One of the easiest ways to find out whether a provider is trustworthy is to research their financial strength rating on one of the rating firm websites. The score will be based on their ability to pay the benefits and their financial health. Here are the top 5 most reliable rating firms:

- A.M. Best – www.ambest.com

- Duff & Phelps – www.duffandphelps.com

- Moody’s Investor Service – www.moodys.com

- Standard and Poor’s – www.standardandpoors.com

- Weiss Research- www.weissrating.com

Look Into the Customer Service Reputation of the Company

The National Association of Insurance Commissioners allows people to look up the customer satisfaction/complaint ratio score. This You can find out a provider’s customer dissatisfaction and complaint ratio grade on the National Association of Insurance Commissioners (NAIC) website.

Research Your Agent Information

You as a customer have the rights to look up your agent’s credential, licensing, and complaints information:

Credentials – You can find this information on your agents and brokers’ business cards. The titles following their names will allow you to find out the degree they have, and the titles they have earned in certain groups.

Licensing – Ask for your agent and broker’s licensing information. Make sure that they are legally licensed to operate in your state. You can verify the information by searching on the NAIC Consumer Information website or calling your local state insurance department.

Complaints – The NAIC Consumer Information website also supplies any complaint information concerning your agent and broker. Other ways to find out more about your agent or broker is to search on the Better Business Bureau website, search on Yelp, or just make a google search.

Here are some direct warning signs of a sketch agent or broker:

- They recommend you to use your cash value from your existing policy to fund a new coverage plan for more financial gain.

- They advise you not to notify of your current provider about your change or replacement.

- They recommend you to secure a portfolio in someone’s name.

- They ask you to sign blank or incomplete forms and checks.

- They pressure you to buy a certain type of contract.

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

List of Best Providers in the United States

With so many companies to choose from, it is hard to window shop one by one until you decide on your choice. To make the selection step easier, here are some of the biggest and highest-rated companies in the industry. If you are wondering about the rating scale, you should only consider providers that are in the superior (A++ to A+), excellent ranks (A to A-), and good ranks (B++ to B+).

| Ranking | Company | BBB Rating | AM Best Rating | JD Power Rating |

|---|---|---|---|---|

| 1 | State Farm | B | A++ | 828 |

| 2 | New York Life | B- | A++ | 828 |

| 3 | Nationwide | A+ | A+ | 806 |

| 4 | Northwestern Mutual | A+ | A++ | 799 |

| 5 | Mass Mutual | A+ | A++ | 780 |

| 6 | Metlife | B- | A+ | 779 |

| 7 | Principal Financial | A+ | A+ | 774 |

| 8 | Prudential | A | A+ | 770 |

| 9 | Mutual of Omaha | A+ | A+ | 766 |

| 10 | Guardian Life | A+ | A++ | 760 |

| 11 | AXA Equitable | A+ | A+ | 752 |

| 12 | Lincoln Financial | A+ | A+ | 744 |

| 13 | Protective | A+ | A+ | 742 |

| 14 | John Hancock | A+ | A+ | 739 |

| 15 | Transamerica | A+ | A+ | 719 |

| 16 | AIG | A+ | A | 718 |

| 17 | Primerica | A+ | A+ | 717 |

| 18 | Pacific Life | A+ | A+ | N/A |

| 19 | Banner Life | A+ | A+ | N/A |

| 20 | SBLI | A+ | A+ | N/A |

| 21 | Brighthouse | A+ | A+ | N/A |

Best Choices for Smokers

- Transamerica

- American General

- Assurity

- Nationwide

Top Guaranteed Policy Companies

These companies tend to be much friendlier towards individuals with diabetes and some other pre-existing medical conditions.

- American Amicable

- American National

- Assurity

- Fidelity

- Foresters

- Gerber

- Mutual of Omaha

- North American Company

- Phoenix Life

- Principal Financial Group

- Sagicor

- SBLI

- Transamerica

Tips for Lowering your Premium

- Get it young and healthy. People rarely think about their deaths when they are young and healthy. Some parents even open an assurance package for their children who are in their early 20s so that they can enjoy the low rate for the rest of their lives. What is more is that their investment portfolio will enjoy an early start as well. It is something to consider if you are planning how to invest your money. This way, you can also secure the living situation of your children’s love ones in the future.

- Ditch unhealthy habits. If you smoke, it can save you some money by quitting now. By telling the company that you have quit smoking for just 1 year can already somewhat lower your premium. And the longer you have been a non-smoker, the greater the savings. But do not lie that you have quit. If your death unfortunately does link to smoking-related illnesses and the provider finds out you have never quit, they can null the whole contract without refunds.

- Switch Up. If you want a permanent plan but cannot afford one in your current financial status, look into a term contract that will allow you to switch over in the future.

- Start exercising and eat healthy. That is the simplest thing you can do to lower your rate. By having a healthy weight and amount of fat can drastically decrease your premium. In addition, if you have normal range of blood glucose and pressure level, you will be viewed as the lowest risk group and rewarded with a great deal.

- Bundle up. If your provider offers other type of insurance (e.g. auto, home, business, health), consider bundling up your coverage plans for a discount deal.

- Ditch your exciting hobbies. This is the time when you get rewarded for being “normal”. By having a relatively safe lifestyle and hobbies will allow you to get a better price on your life coverage.

- Consider low-load coverage. “Low-load” plans can be purchased from financial advisors. They usually do not include agent commissions and tend to more affordable than usual coverage plans purchased from an agent.

- Do not waste your time with guaranteed plans if you are healthy. Guaranteed packages do not require medical exams but require a higher premium cost. If you are healthy, you may as well go through with the physical exam and enjoy a lower rate.

- Opt to pay your premium in one payment annually. Usually companies will give you a discount by paying your premium annually in one lump sum than in installments. Throughout the years, if you continuously take 10 to 20% off your annual premium, that can really add up if you have a high value plan.

- Ask reevaluation after health improves. You can always purchase a plan, improve your health by exercising and cutting off bad habits and ask for another physical exam to prove that you are health-conscious to the company. By seeing the improvement, your insurer will likely lower your rate as a reward.

- Go with more local companies. Because they have less company expenses, they will have a friendlier price for their packages.

How Does The Claiming Process and Payout Work?

After the insured person has passed on, the heirs can file a claim with the insurer by submitting the loved one’s certified death certificate. According to the state’s life insurance regulation, the company will have 30 days to process the claim. Within this time limit, they must decide to pay it, request for further information, or deny the claim by sending a written letter to the beneficiaries along with a detailed explanation concerning the reasons on which the rejection of claim were made. Depending on the state’s regulation, the provider must pay within 30 to 60 days from the claim date.

What Circumstances Can Postpone the Payout?

There are a number of reasons the insurer can delay the payment of death benefits. Here are the most common situations:

- The insured passes away within the contestability period (usually 2 years from the plan’s effective date). In this scenario, the insurer will have the right to investigate thoroughly whether your loved one has supplied any incorrect or omission of information in the application. If yes, they can use this reason to deny your claim. But if they cannot prove any falsification of information, they must pay. This investigation can delay the payment by 6 to 12 months.

- The circumstances of the death can also delay the payment. If the insured’s cause of death is listed as homicide, the agent will have the right to contact the assigned detective and gather evidence to decide whether your loved one died was accidental or result during the process of committing certain illegal activity. If the insured died while committing criminal activity, the claim will be denied. And in the circumstances where the beneficiary is listed as a suspect, the payout will be delayed until they are cleared of the suspicion or acquitted from the crime before the insurer proceed with the payment.

Payout Options

Traditionally, the benefit is paid to the heirs in 1 payment. However, since 5 years ago, the method of installment payment has been introduced as a new payment option. You may wonder why would anyone want their recipients not to get the whole amount of money all at once? If you think about giving a huge amount of money to a very adult, you can imagine how easily they can waste away the money quickly. To avoid this problem, the insured will have the right to decide how the money will be paid out to the recipient while the rest of the cash value remains in investment portfolio for further growth.

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

5 Most Common Reasons Insurers Deny a Claim

- Your death occurs in the contestability period. All life coverage have a contestability periods that last for 2 years from the date your plan becomes active (it is only 1 year in some states). If you pass away during this period, your company will have the right to check on all the information as written in your application. Any incorrect information will allow them to deny the claim.

- Your death is not covered in the regulation. Death by suicide is the only exclusion in this rule.

- Failure to disclose important personal information. Insurers have the right to deny your claim if they find out that you have intentionally omit important information that play a role in accessing your application acceptance and rate. These information can be not disclosing of a DUI record, your smoking habit, certain illnesses and medical condition, and even owning a race car.

- Death resulted from dangerous activities. Your contract is likely to state what is regarded as a dangerous activity (e.g. skydiving, paragliding, scuba diving, driving a race car, rock climbing). If you do unfortunately die while engaging in one of these activities, your family will not receive the death benefit based on the fact that you have violated the contract rules.

- Non-resident of the United States. This depends on whether your contract has a clause that states you have to be living in the United States at the time of your death in order for your beneficiaries to receive the death benefits. If you do, and your death occurs outside of the country, your provider will deny your claim base on this rule.

Third Option: Life Settlements

If you have purchased a whole life package and you no longer consider it a need, do not terminate the plan immediately. There is a third option to consider – sell your plan to a third party investor. This transaction is called a life settlement. You, as the owner, will receive an agreed upon cash payment in exchange of transferring your ownership of the policy to the investor. The investor will continue to pay for your premium until your death. At this time, the investor will collect the death benefits as your beneficiary.

Is Life Settlement Legal?

Yes, it is perfectly legal. It has been ruled as a customer’s right since 1911 by the United States Supreme Court. According to the federal law, life assurance is a “private asset that the owner should have the right to sell”.

Differences between Life Settlement and Viatical Settlement?

Although viatical settlement and life settlement both have to do with the owner selling their plan to a third party investor, there is one very important difference between the two transactions. Viatical Settlement defines any settlement where the insured sellers are suffering from terminal illnesses and have a life expectancy of less than 2 years. When the cash value and accelerated death benefits are not enough to cover treatment cost and living expenses, subscribers can sell their portfolio for more immediate cash in the meantime. Life settlements are involved with sellers who do not have any terminal illnesses and are reasonably healthy. Please note that there are different regulations concerning these 2 types of transactions.

Who Would Want to Sell Their Policies?

Do you know that of the annual income of approximately $20 trillion from life insurance sector, about 88% of the policies never surface as a claim payout? Here are the top reasons why so many plans are unclaimed:

- The policyholder’s financial status changed and can no longer afford the premium.

- The coverage is no longer necessary (e.g. client no longer need to worry about their spouse as the children now can take care of the parent, the children no longer need the coverage as they are now self-sufficient financially)

- Couples make a purchase on a policy. Years after they have a divorce, and the paying party no longer want to continue with the payment.

Obviously, the providers do not want customers to know of this third option as it means that increasing claims equal to lowered profits. And customers, without knowing of this alternative opportunity, often just request a refund of their cash value or even allow the whole plan to lapse. Instead, you can actually earn thousands for selling your plan to an investor.

Who is Eligible to Sell Their Plan?

In order to qualify for this option, you must be 65 years or older and in relatively good health. In addition, you must have the plan for at least 2 years (or the length of your contestability clause).

What Plans Are Eligible for Settlement?

Almost all types of coverage are eligible: term, permanent, universal, variable, and survivorship life policies. According to surveys, investors find universal life and convertible term life to be the most profitable. Hence, these can go for more money than other types of plans.

How Much Can I Expect from My Settlement?

How much you will recur from your plan depends on several factors such as your life expectancy, the type of plan you purchased, the value of the porfolio, your premium rate, and how many years you have subscribed to this plan. To give you an idea how much you can expect as your cash back, here is a chart of the general average payout for your plan based on your age:

AGE AT ISSUE

35

50

65

80

AVERAGE MAX CASH BACK IN % OF VALUE OF POLICY

5%

16%

26%

52%

Quite interestingly enough, the selling process is the opposite of buying process where you score a better deal the younger you buy. In this scenario, the older you sell your policy and the shorter your life expectancy, the more valuable your portfolio will become. Consequently, the payout will be much higher if you sell later than earlier. And in cases where the holder has less than 2 years of live, the price is much more than those in life settlements.

Where Can I Sell My Package?

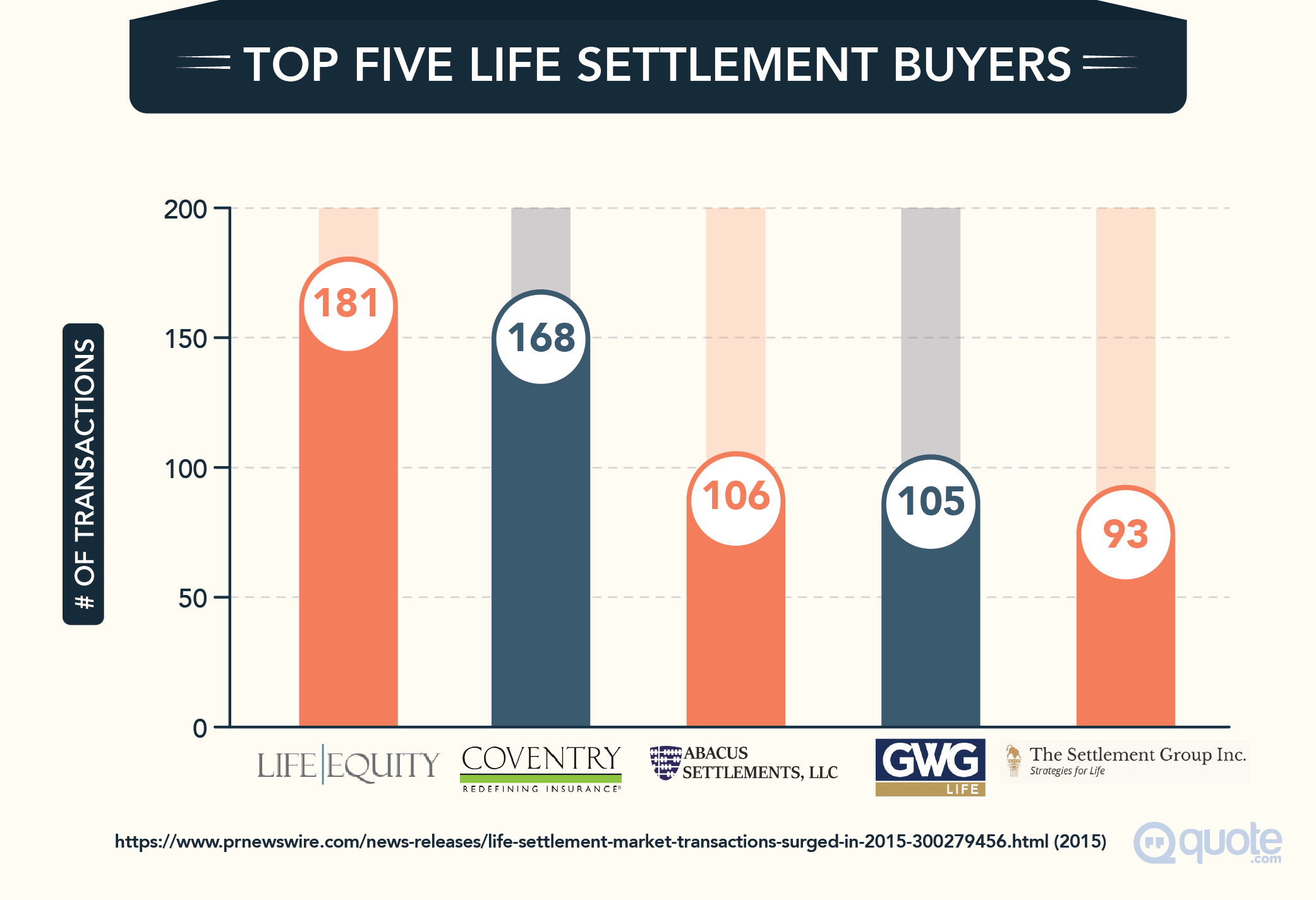

Currently, there are no settlement exchange market in the United States. Most transactions are done in private dealings between buyers and sellers regulated between two parties of brokers similar to real estate trades. often facilitated by two types of life settlement companies. However, the seller and buyer can also opt to represent themselves in the trade. If you are considering selling, you have the option to go with a broker and provider.

Life Settlement Brokers vs. Providers

Brokers functions as a representative on your behalf to settle a price and terms with an investor buyer. They work as a collector of offers from various parties and presents them to you for your choosing. This way, you can have the upper hand of getting a higher value in the trade than negotiating directly with one investor. Note that if you decide on working with a broker, the process of obtaining offers is usually free and not legally binding. However, once the terms are confirmed and the transaction is made, the broker will charge a commission fee for the deal. On the other hand, you always have the option to work directly with a provider and benefit from the omission of the commission fee. Life settlement providers are licensed firms that buyout portfolios for large organized investors. Sometimes, they act as the middleman; other times they are the investor themselves. So this becomes a game of negotiation to see who will offer the best deal and whether you will need to pay commission or not. If you wish to explore both parties, here are some examples of reputable life settlement brokers:

- Ashar Group: www.ashargroup.com

- Ovid Life Settlements: www.ovidlife.com

- Policy Options Life Settlements: www.quicklifesettlements.com

- Welcome Funds: www.welcomefunds.com

Examples of the top providers:

- Coventry Life Settlements: www.coventry.com

- GWG Life Settlements: www.gwglife.com

- Legacy Benefits, LLC: www.legacybenefits.com

- Life Equity LLC: www.lifeequity.com

- Magna Life Settlements: www.magnalifesettlements.com

- Settlement Group, Inc: www.lifesettlementgrp.com/

Something to Consider About Settlements

As with any selling of investment, there are always some essential considerations to know about before talking with any parties whether it is brokers or providers to avoid being taken advantage of. Here are a list of issues you must identify:

Transactional Fee – There is a transactional fee on top of any settlement case. Your state’s insurance regulation have a maximum percentage fee enforcement on all trades. However, the provider and broker may set a lower percentage. Either way, they should also disclose this information up front. If anyone try to tell you a charge higher than the state’s maximum fee, it is a clear sign that they are trying to take advantage of you.

Transparency in Deal – If you feel that at any point there is something uneasy about the deal, stop. Ask for second opinion from other professionals. A professional broker should never intimidate or pressure to choose one offer over another. They should also never recommend that you accept the first offer to come so that they can get paid sooner.

Importance of Privacy Policy – Because the contract has so much of your personal information, you need to make sure that your broker will send only the necessary information to quote offers without exposing your intimate data. Remember, your broker should not send your information to anyone without requesting for your permission. To ensure this rule is being enforced, you should ask to attain a full privacy procedure from any broker before handing over any of your information. Once you have this contract, the broker is legally bind to treat your private information with upmost caution.

Impact on Your Financial Status – Remember that the transaction payout is different from a payout in that it is taxable and is regarded as income. The sudden influx of money ca affect your eligibility to certain public assistance programs such as Medicaid and old age pension. Before you go ahead with the deal, make sure you are fully aware of the impact on you and your spouse. If you have any uncertainty, you should consult with your lawyer, accountant, or any other financial aide.

Impact on Your Beneficiaries – Even if you decide that you no longer need the coverage, you should consult with the intended benefit receiver. Ask them if they would like to keep the package and pick up the premium payments. This is often a better way to utilize the plan as an investment instead of recouping your money through selling the contract.

Importance of Financial Advisor

Usually when you notify that of your interest to your provider, they will seat you down with a financial advisor to go over your portfolio and all the options available. Unlike a broker and provider, they solely have your best interest as their priority and want to help you find the best solution. They will usually go through this process:

- Inquire why you wish to terminate your package.

- Go over all the possible options in solving your current circumstances. For example, if you wish to quickly gather a large sum of money, they may evaluate whether it would be more beneficial to apply for a personal loan, remortgage certain assets, or sell your policy. Each option will be weighed based on their advantages and disadvantages.

- If at the end, the advisor comes to the conclusion that settlement is the correct approach, they would recommend a broker or provider that will work with you for the rest of the process.

- At any point you need any second opinion, they should be available to assist you with your concerns.

Life Settlement Contract Process at a Glance:

If you do decide to go ahead with the deal, here is a summary of how the deal will proceed:

- Advice — A financial advisor will go over your case to confirm this is the best choice.

- Broker Inquiry – You should meet with several broker and decide on one to work with. This is when you should ask for a privacy contract from the broker before you hand over all your personal information.

- Information Assembly — The broker compiles all the relevant information about your policy and your medical health records. From the information, they should consult with a life expectancy underwriter to estimate how long you will be alive.

- Application— You will need to fill out a sale application for the sale before the broker send the information to different providers.

- Wait—It will require some time before your broker returns with offers from various providers. This can take a little time as the providers need to run your numbers and crunch out their margin of profits, risks, and other necessary data in order to send back an offer.

- Evaluate Your Offers—Your broker will show all offers sent back to you. Along with the advisor, they will go over all the offer with you and make sure you understand the contract in each. You will a limited amount of time to consider all the offers (the duration is usually 30 days). Once you decide on an offer, your broker will contact the provider with the news.

- Completing the deal—The provider will send back a transfer contract and closing package that contains all the necessary documents to seal the deal. Your broker will go over the documents with you and answer all your questions and concern with unclear statements. Your advisor should also be in there to consult you of any concerns or sketchy statements.

- Submitting the Escrow—Once you sign all the forms, your broker will submit all the paperwork to an escrow agent safekeeping until the provider send you the cash payment.

- Acknowledgement of Ownership Transfer— After the provider receives the paperwork and release the funds to the escrow agent. The agent will then transfer the funds into your bank account to complete the whole process.

FAQ

Will my policy get cancelled if I miss a payment?

This question depends on whether you have a term or whole policy. For term plans, you have a grace period to pay your premium. After the period, your company will have the right to drop your coverage. As for whole protection packages, as long as you have saved up cash value, your company will use the accumulated money to cover your premium until it runs out. Afterwards, if you do not pay within the grace period, it will be canceled. Because each state has its own regulation regarding grace periods, please check with your state agency to confirm the duration as it can vary from 10 days to 30 days.

When should I consider buying a life portfolio?